Wake Up Call

“The stock market is a device for transferring money from the impatient to the patient…” – Warren Buffet

Since the beginning of February, we have witnessed a surge in long-term bond yields. The 10-year Treasury yield has moved from 1.1% to as high as 1.75% and yields on the 30-year have gone from 1.8% to as high as 2.5%. In percentage terms, long-term interest rates have moved by as high as 60% since the beginning of February. Moves like these are not normal, and on a statistical basis occur in less than 5% of all observed cases (2.6 standard deviation move during February alone). The last time we saw moves this big was when President Trump was elected and during the Taper Tantrum of 2013 (Chart 1 below)[1].

Chart 1

Given that equities are receiving a wakeup call from the bond market, it feels like an opportune time to assess the interest rate environment, how interest rates affect equities, and ultimately whether the recent weakness warrants concern.

Interest Rate Environment

Theoretically, long-term interest rates are driven by two factors: GDP expectations and inflation expectations. Each of these factors have been on the rise since 2021 began. Goldman Sachs revised their GDP estimates higher last month from 6.6% to 6.8% and the ten-year inflation expectations have risen from 1.6% to 2.3% since the beginning of February[2].

In practice, external factors also drive interest rates. At the moment, interest rates are being forced lower by two meaningful forces: the Federal Reserve and the global “hunt for yield”. Back in March of 2020, the Fed re-ignited and expanded their crisis era bond buying programs in response to the “corona-crisis”. These actions have provided confidence to the market, and with a new buyer with very deep pockets in the space, yields on everything from government bonds to high yield corporates have fallen to pre-pandemic lows. Further, global investors have been on the “hunt for yield” since quantitative easing (“QE”) programs went into effect following the Global Financial Crisis of 2008. Since 2015, whenever U.S. 10-year rates have gotten a whisker above 3%, investors were quick to buy in and drive rates lower (see chart 2 below).

So how should we characterize the current interest rate environment? First, let’s acknowledge that long term interest rates are really, really low relative to history (Chart 2 below). This is a highly accommodative influence with several positive effects for consumers and corporations. Second, although the fundamental factors that support higher rates are certainly in place, the market dynamics mentioned above should keep a lid on any significant move higher. We have already heard whispers of “Operation Twist 2.0” and with bond yields at century lows, the “hunt for yield” shows no sign of abating. Considering all of these factors, we would argue the interest rate environment is highly accommodative.

Chart 2

How do Rates affect Equities?

The impact of higher rates on the equity market is mixed. As rates rise, bonds become more attractive to investors as they receive greater compensation for lending their money. That reduces the attractiveness of equities, as investors require a higher return to entice them away from the safety of higher interest-bearing bonds. From a fundamental perspective, rising rates equate to rising borrowing costs. Unless businesses can pass those onto the consumer, it could hurt earnings and reduce multiples. Rising interest rates are not all bad news, however; at certain levels they are a signal of strength in the economic environment and act as a governor on capital allocation decisions.

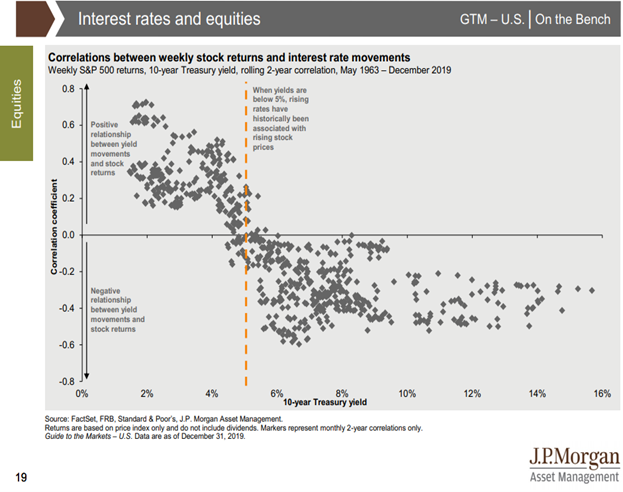

So, when are increases in long term interest rates a positive or negative for equities? According to our friends at J.P. Morgan, the magic number is somewhere around 5% (See Chart 3, below). When long term yields are below 5%, rising rates have historically been associated with rising stock prices. Presumably at these levels, rising rates are indicative of an economy operating in a healthy manner which should be good for earnings. Once rates pass the 5% level, equity returns become negatively associated with interest rate movements. Presumably at these levels, interest rate increases are a hindrance to earnings, or bonds are simply becoming more attractive relative to equities. If history is a guide, we can comfortably say that we have quite a bit of room to run before rate increases on long-term bonds become an issue for equity markets.

Chart 3

Is the Recent Weakness Cause for Concern?

Markets have been weak since the back-up in rates really took off. Although the S&P 500 hit all time highs this week, any surge in rates has been cause for weakness in equity markets. Is this weakness just a normal correction or the start of something more sinister? We develop our mosaic by looking at a lot of factors, but a few items have stuck out over the last few weeks which should provide some comfort in classifying this is a normal correction.

First, credit spreads are very tight. If the recent weakness is related to the fundamental strength of corporate borrowers, it should show up here, and it has not (Chart 4 below). Second, I’d point out that going back to 1980, an average intra-year drop for the S&P 500 is 14%. As of the middle of March, the worst performing index (Nasdaq) had fallen 7% from its peak in price return terms, still within the bounds of “normal”. Third, in 31 of the 41 annual periods tracked on the chart below, returns were positive despite experiencing meaningful drawdowns (Chart 5 below). In other words, it would be odd if markets did not experience some weakness during a given year. Considering the above points, it leads me to believe the current weakness is normal rather than something more concerning.

Chart 4

Chart 5

What I hope you take from this commentary is we believe the weakness we are seeing today is occurring in response to the velocity with which rates have moved higher. Markets don’t like uncertainty, and a near three-standard deviation move in interest rates is certainly cause for surprise. Still, the long-term interest rate environment is very accommodative, equities are still behaving in a normal fashion, and using history as a guide, small bouts of weakness are essentially guaranteed. With all that being said, we remain steadfast in our messaging; getting invested, remaining invested and using opportunities like these to acquire shares in great companies is the most repeatable method to grow your wealth.

Sources:

[1] Goldman: U.S. Weekly Kickstart “Rates Rise, Equities Fall…” – Kostin, et al.

[2] Goldman: U.S. Daily: “A Bigger Stimulus Bill and the Process From Here” – Hatzius, et al.

Disclosures: All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

New World Advisors, LLC ("New World") is a Registered Investment Advisor (“RIA”) with the U.S. Securities and Exchange Commission (“SEC”). Advisory services are only offered to clients or prospective clients where New World and its representatives are properly licensed or exempt from licensure.