Q1 2024 Market Commentary

Market Recap

It was a notable start to 2024 as the momentum from the final two months of 2023 carried forward. The S&P 500 Index increased +10.2% for the first quarter of 2024, marking the best start to the year since 2019, and the 14th best since 1926.[1] Global stocks as measured by the MSCI ACWI rose +8.20% for the quarter.[2] Stock market gains were broad-based, with all major MSCI country indices, equity asset classes, and most S&P 500 sectors ending the quarter higher.

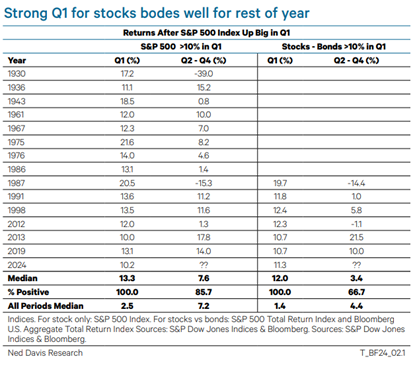

History suggests that such strong starts to the year for the S&P 500 have led to additional gains for the remainder of year. The table below shows that when the S&P 500 rallies at least +10% in the first quarter, it has continued to rise 85.7% of the time over the final nine months of the year by a median of +7.6%. While there have been exceptions, the overall trend suggests a positive outlook for stocks.

Unlike late-2023, bonds as measured by the Bloomberg U.S. Aggregate Index slipped -0.8% during the quarter. The first quarter outperformance of stocks compared to bonds was significant, with the S&P 500 beating the Bloomberg U.S. Agg by 11% on a total return basis, the most since 2012.[3]

Factors such as sticky inflation, resilient economic growth, and the repricing of when and how many Fed interest rate cuts soured investors on bonds. In March, the Federal Reserve’s decision to keep interest rates unchanged underscored a patient approach to monetary policy. While there was a slight shift in the dot plot by the majority of FOMC members with fewer rate cuts in 2024, the overall tone suggests a gradual easing of policy. The Fed’s stance reflects its dedication to maintaining a delicate equilibrium between the objectives of supporting sustainable economic growth while guarding against inflationary pressures.

The Fed’s preferred inflation gauge of Core Personal Consumption Expenditures (PCE) remains elevated at 2.8%, surpassing the 2% target, which could have several implications for financial markets. First, the central bank may opt for fewer rate cuts over the next year than previously anticipated. Second, the Fed might choose to wait until later months, such as June, to further assess the trajectory of inflation and its impact on the economy before acting. Third, the Fed is likely to adopt a more gradual and cautious approach to easing monetary policy. In aggregate, this may be beneficial for the stock market. The chart below shows that a slow easing cycle has historically been positive for stocks, as it provides continued support for economic growth without causing abrupt disruptions.

Current Positioning

Our asset allocation framework continued to improve as the year began. In response, we increased the U.S. equity exposure across portfolios and reduced bonds during January. As highlighted in the chart below, the probability of a global recession appears low with a soft-landing environment as the base case scenario for the U.S. While U.S. economic growth is projected to moderate this year, labor markets remain resilient, earnings growth is forecasted to accelerate, and overall inflation is expected to continue to trend towards the Fed’s long-term target. These are positive factors which support the market’s expectations of a Fed pivot and interest rate cuts later this year.

During the quarter, the modest reduction in the bond allocation came from the short-duration bond position. The goal of this change was to maintain the income profile and diversification benefits of longer-duration bonds in portfolios, while preserving the defensiveness of the bond allocation given that the interest rate cycle is near a peak. Furthermore, we believe it is important to reiterate that as we near the end of this hiking cycle, the opportunities embedded in bond market dynamics, especially given the economic backdrop, are truly historic for investors. History has shown that yields begin to decline in the two to three months before the first rate cut. As a result, our strategy has been to invest in the areas of the bond market that will benefit from this shift by extending the duration of bond portfolios and keeping strategic cash at a minimum.

Technical Market Factors we monitor continue to exhibit long-term strength and have remained resilient during any pullbacks. As noted earlier, market breadth has continued to improve, and this reinforces an overall healthy environment for equities. While the elite eight tech companies were the standouts for much of 2023, the chart below highlights how the relative performance of the S&P 500 has begun to broaden out to the remaining 492 companies in the index. While the market will experience pullbacks, the drivers of longer-term market performance remain in place.

Investor Sentiment has rebounded since October of last year with optimism rising. While short-term sentiment indicators could leave the market susceptible to disappointments, any pullback in optimism would be positive for stocks. Consumer confidence is less optimistic, while money market assets remain at record levels supported by monetary policy. We believe this will shift and provide additional fuel for equity markets once the Fed pivots and begins to cut short-term rates.

Outlook

Entering the second quarter, we maintain a neutral weight relative to our strategic global benchmarks. Within U.S. stocks we are particularly positive on small caps to the detriment of our international exposure. A prospective environment of declining interest rates and inflation should provide a tailwind for U.S. small caps. Beyond that, small-caps have been unloved and are historically attractive, trading near a 20-year low relative valuation compared to large-caps. Given the resilient investment landscape, we anticipate the opportunity to increase the exposure to stocks on short-term volatility. We anticipate that the formal shift in Fed policy toward an easing cycle will take place this summer to avoid any appearance of influence or partiality ahead of the Presidential election this fall. The remainder of the year will likely bring with it moderate job gains, easing inflation, and ultimately a favorable environment for the U.S. economy to navigate towards a soft landing.

[1] Morningstar Direct

[2] Morningstar Direct

[3] Ned Davis Research